Physician mortgage loans are designed for doctors and certain medical professionals who may have high student loan balances or limited savings early in their careers. These programs can use flexible underwriting to account for contract-based income and employment stability.

This guide explains how physician mortgages work, typical requirements, costs to expect, and how physicians decide whether a physician program or a conventional loan is the better fit.

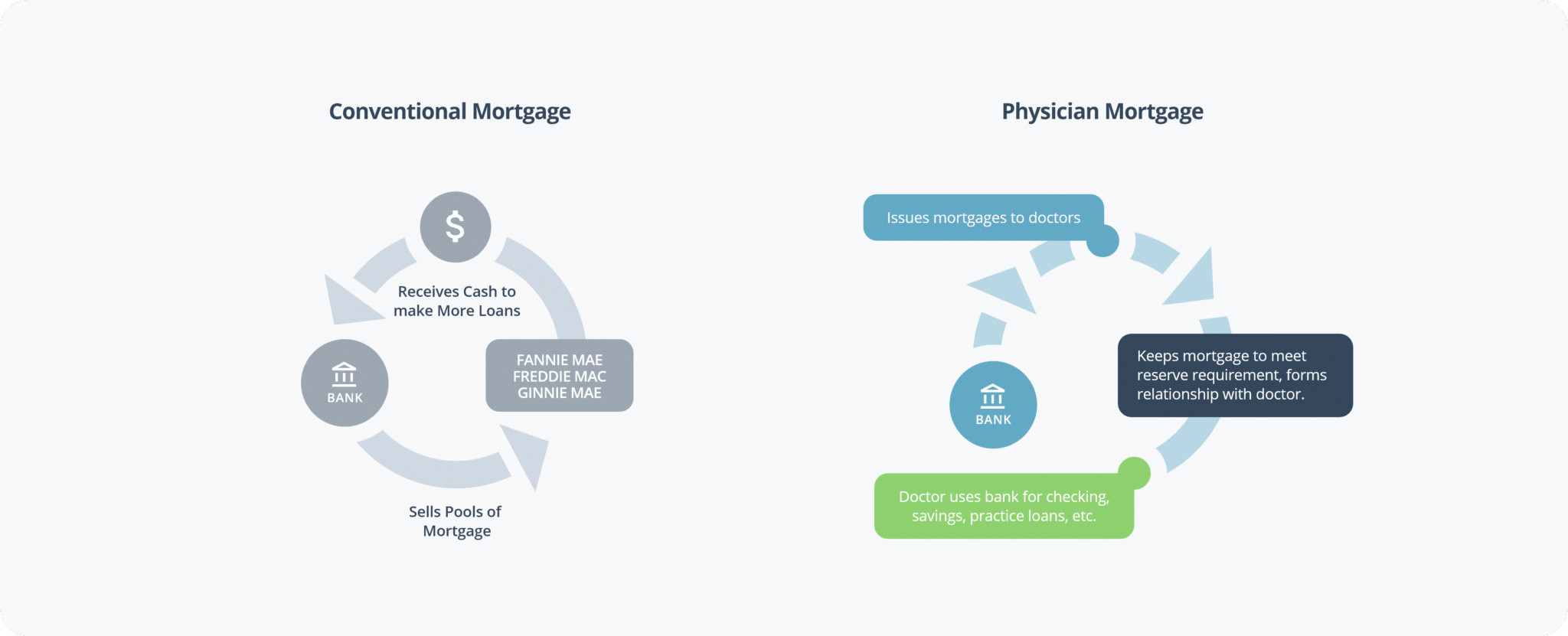

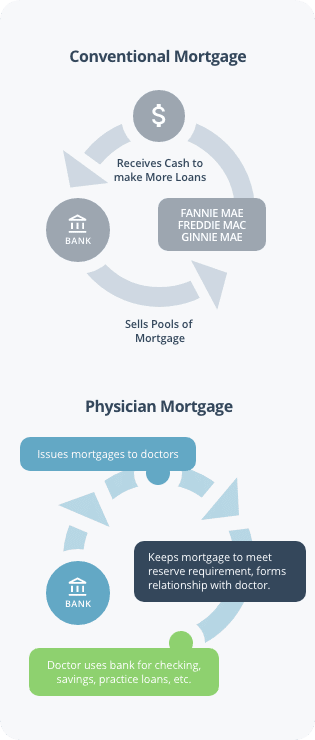

What Is a Physician Mortgage Loan?

A physician mortgage loan is a home loan program offered by select banks and lenders to physicians and other eligible medical professionals. While each program is different, the general idea is consistent: a lender may evaluate a physician’s application using a broader view of future earning potential and job stability than a standard conventional mortgage.

This matters because many physicians buy a home during a transition, after residency, during fellowship, or shortly after starting an attending role. At that point, savings may be thin, employment history may be short, and student loan balances can make a conventional application look worse than the reality of the borrower’s long-term financial outlook.

A physician mortgage is not automatically better than a conventional loan. It is simply another option, and it should be compared based on rate, fees, structure, and how the lender treats student debt.

How Physician Mortgage Loans Work

Physician mortgage programs are not standardized across the industry. Two lenders can both advertise “physician loans” and still have meaningfully different rules on eligibility, down payment, loan limits, and documentation.

Most physician mortgage programs are designed around a few underwriting concepts:

Contract-based income

Many programs allow a signed employment contract to support income qualification, even if the start date is in the future. That can help physicians who are relocating or starting a new position but have not yet built a long W-2 history at the new job.

Student loan treatment

Student loans can drive a physician’s debt-to-income ratio higher than conventional underwriting prefers. Some physician programs evaluate student loans using the required monthly payment (such as an income-driven repayment payment) instead of a larger calculated payment. Others may apply their own approach. The details matter, and this is one of the biggest reasons physicians compare programs rather than assume approval.

Credit and cash reserves

Physician programs still care about credit, assets, and overall stability. A strong credit profile and clean history can improve approval odds and pricing. Some lenders also have reserve expectations depending on the loan size and property type.

Primary residence focus

Most physician mortgage programs are intended for a primary residence. Property requirements can vary, and some lenders are more restrictive on condos or certain property types.

Because these rules vary by lender and state, the main advantage of a physician program is often not a single feature, but that it can offer a workable path to homeownership when a conventional loan is not the cleanest fit.

Physician Mortgage Loan Process

The process of getting a physician mortgage usually looks similar to a conventional mortgage, but the documentation and underwriting questions can differ.

1) Application and initial documentation

You provide basic financial information, permission for a credit pull, and documentation such as assets and employment details. If you are qualifying with a contract, the lender typically reviews that contract closely.

2) Preapproval

If the lender is comfortable with the initial profile, they issue a preapproval that outlines the price range you may qualify for. This helps you shop realistically and strengthens an offer when you find the right home.

3) Offer and contract

Once you make an offer and it is accepted, the lender moves the file into deeper underwriting. At this stage, timelines, documentation, and property details start to matter more.

4) Appraisal and underwriting

The lender orders an appraisal to confirm the property value and completes underwriting. Underwriting is where most conditions show up, especially around income documentation, assets, student loans, and any credit questions.

5) Closing

After conditions are cleared, you sign closing documents, fund the loan, and take ownership. Your closing costs and prepaids are finalized here.

The main thing physicians should plan for is that “physician loan” does not mean “no underwriting.” The program may be more flexible in specific areas, but it still requires a complete file.

Typical Costs of a Physician Mortgage Loan

Physician mortgage loans generally have the same cost categories as other mortgages, but the total cost can differ depending on program structure.

Closing costs

Closing costs often include lender fees, appraisal, title insurance, escrow setup, and other standard mortgage expenses. These costs vary by state and lender, and they can be influenced by whether the loan is jumbo-sized.

Monthly payment components

Your monthly payment typically includes principal and interest. Many borrowers also pay property taxes and homeowners insurance through escrow, depending on lender requirements and down payment.

PMI and rate tradeoffs

Some physician mortgage programs do not require PMI, which can reduce monthly cost compared to a conventional loan with a low down payment. However, that benefit can be offset if the physician program has a higher rate or higher fees. The correct comparison is total cost, not a single feature.

Structure matters

Some physician programs use adjustable-rate mortgages. An ARM can be appropriate in some situations, but it introduces rate-change risk. Physicians should evaluate how long they plan to stay in the home and whether the payment remains affordable if rates adjust upward.

If you are comparing a physician program against a conventional loan, focus on the full package: rate, fees, required down payment, PMI, and whether the loan structure fits your timeline.

Who Qualifies for a Physician Mortgage Loan?

Eligibility is lender-specific, but physician mortgage programs usually target medical professionals who have stable employment prospects and a strong income trajectory, even if their balance sheet is still catching up.

Many lenders focus on:

- Degree and credential requirements (varies by lender)

- Career stage (some prefer early-career, others allow established physicians)

- State availability (not every program is offered everywhere)

- Credit profile and overall stability

- How student loans impact debt-to-income calculations

- Property type and occupancy (usually primary residence)

The key point is that qualification is not just about being a physician. It is about whether the specific program fits your degree, state, and financial profile.

Benefits of a Physician Mortgage Loan

Physician mortgage programs can be useful when they solve a real friction point in the home-buying process.

Lower down payment pathways

Some programs allow low down payments, which can help physicians who are relocating or prefer not to drain reserves right after training.

PMI avoidance in some programs

Some physician mortgages do not require PMI, which can improve monthly affordability compared to a conventional loan at a similar down payment.

Contract-based qualification

For physicians starting a new role, the ability to qualify using an employment contract can remove a timing barrier that shows up with conventional underwriting.

High loan amounts for expensive markets

Some programs support higher loan limits, which can matter in high-cost areas. That said, a higher limit is not automatically a benefit if it pushes you beyond a comfortable payment.

Drawbacks of a Physician Mortgage Loan

Physician programs can also introduce tradeoffs that are easy to miss if you only focus on “low down payment” or “no PMI.”

Adjustable-rate risk

Many physician mortgages are structured as ARMs. If rates reset higher, the payment can rise. That risk needs to be planned for, not ignored.

Higher pricing in some cases

Some physician programs have higher rates or fees than a strong conventional borrower could get. The only way to know is to compare side by side.

Over-borrowing risk

Higher loan limits can tempt buyers into an expensive home before their budget is stable. This is especially relevant during early attending years when income, lifestyle, and location can still change.

Primary residence limitations

Most programs are designed for owner-occupied homes and may be restrictive on investment properties or certain property types.

Alternatives to a Physician Mortgage Loan

A physician mortgage is not the default answer. Depending on your profile, alternatives may be better.

Conventional loans

If you have a strong credit profile, stable income history, and enough down payment to avoid expensive PMI, conventional financing can be competitive.

FHA loans

FHA can be attractive for some buyers because of lower down payment requirements, but mortgage insurance costs and loan limits can make it less appealing for many physicians, especially in high-cost markets.

Piggyback loans

Some buyers use a first mortgage plus a second loan to reduce the down payment burden or manage PMI, but this structure introduces complexity and sometimes a higher blended rate.

Refinancing later

Some physicians use a physician mortgage early, then refinance into a conventional loan after income stabilizes, student debt changes, or equity increases. Whether this is smart depends on rates, fees, and how long you plan to keep the home.

How Physicians Decide Between Mortgage Options

Most physicians choose a mortgage by comparing total cost and flexibility, not by chasing a single feature.

A practical decision framework looks like this:

- Compare rate and fees across both physician and conventional options

- Understand whether the loan is fixed or adjustable, and what happens after the initial period

- Evaluate down payment requirements and whether PMI applies

- Confirm how student loans are treated in underwriting, using your real repayment terms

- Stress-test the payment against your budget, especially if rates adjust or income changes

- Consider timeline, how long you expect to stay in the home, and whether you may refinance

LeverageRx can be used as a comparison starting point to help physicians see which lender programs may fit their state and credential, then confirm details directly with a loan officer.